Are 100-Year Mortgages Next? Effects of Negative Real Interest Rates on Nordic Housing

Bubble

by Nick Kamran • Mar 4, 2017

Wage Growth vs. Housing Price Growth

By Nick Kamran, an American living in Oslo, Letters from Norway:

Historically, central banks throughout Europe had one mandate: price stability. They did not worry about employment or economic growth, only currency integrity. Setting interest rates to contain inflation ensured that a Krone or a Euro would purchase tomorrow what it could today. Nevertheless, since the ebbing of the 2008 financial crisis, The ECB, of which Finland is a member, officially added full employment and economic growth to their mandate. The Norwegian, Swedish, and Danish Central Bank’s followed suit, stating that they would consider “other factors” than inflation when basing an interest rate decision.

Hence, instead of remaining impartial — leaving it to lawmakers, markets, and the public to deal with the prevailing interest rate — the central banks became involved in policy making. Adding employment and economic growth to their mandate equates to the National Institute of Standards changing the definition of the meter to help an engineering firm, working on a major bridge project, meet budgetary and timeline constraints. In addition to creating a dilemma, the additional mandates made central banks appear politically biased.

The Conundrum

In an attempt to balance, what central bankers perceive as two opposing forces, inflation and unemployment, they chose economic stability over maintaining price stability. The other option, raising rates would have led to greater short-term unemployment. The central banks pushed benchmark rates all the way down, nearing zero in Norway (.5% – Key Policy Rate ) and Denmark (.05% – Discount Rate), hitting it in Finland (ECB at 0% – Refi Rate) and going negative in Sweden (-.5% – Repo Rate).

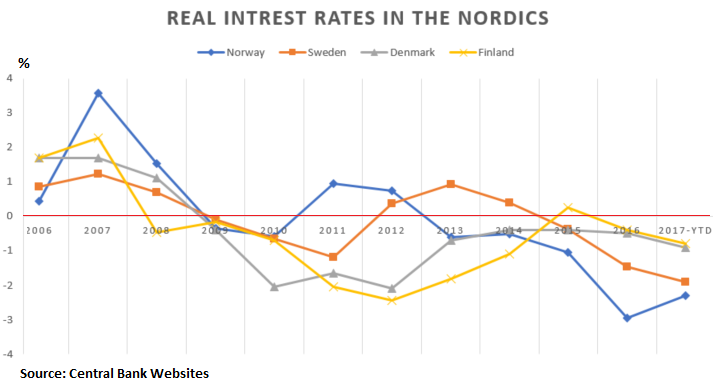

Note that central-bank deposit rates are even lower, and negative, to force money out of the banks and into the economy, stoking inflation. Currently, the real interest rates – key interest rates minus inflation — are deeply negative for all the Nordic countries.

Although the policy mostly kept unemployment at bay, relative to historical levels in the respective countries: currently at 4.4% in Norway, 7.3% in Sweden, 4.2% in Denmark, and 9.2% in Finland, it inflated a housing bubble. In Norway and Sweden, where real interest rates are especially negative (-2.3% and -1.9% respectively), housing prices inflated the most. In Oslo and Stockholm, the trend continues.

Wage vs. Housing Price Growth

From 2007-2016, professional wages grew, in local currency, 40% in Norway, 32% in Finland, 25% in Sweden and 24% in Denmark. During roughly the same period, apartment prices, in local currency and on a per square-meter basis, surged 107% in Stockholm, 93% in Oslo, and 38% in Helsinki. Copenhagen area, overall, only went up 8% during the same period. However, in recent years, they experienced a surge as well.

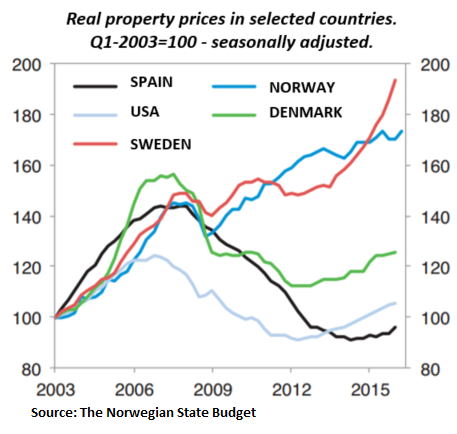

Taking the difference, housing price rise minus wage increases, discounting salary hikes, we can see that housing rose 82% in Stockholm, 53% in Norway and 6% in Finland. In Denmark, wage growth outpaced housing by 16% in the same period. The chart below, taken directly from the Norwegian State Budget, further illustrates the Nordic housing markets compared to other major western markets. Using indexes and accounting for the whole country, we clearly see that Norway is lifting-off and Sweden is going parabolic.

Are 100-year mortgages next?

Finland and Denmark, the Nordic countries with the least negative rates, experienced the least housing price growth. Wage growth did not keep up with housing prices, (except in Denmark), further illustrating that negative interest rate policy, in general, which intends to go all out for growth, does not properly stimulate the economy and does not promote sustainable growth across all sectors.

The Nordic case clearly illustrates that central banks should only maintain price stability which upholds currency integrity. The rates, when correctly managed, act as a regulator, ensuring the economy remains diversified. No one sector can take all the growth. The “negative (real and deposit) interest rate” experiments are failing. They’re distorting the economies which undertook them. Surging housing costs are aggravating inequality and depriving other sectors in the economy. For example, retail sales since 2007 in Norway grew only 8% despite a brisk population increase (up 11% over the same period) and expanding consumer credit (up 13%).

Sweden and Norway are already deep into the bubble; housing continues to outrun inflation and wages at an alarming rate. Helsinki outpaces the rest of Finland but remains in check due to unprecedented construction of new housing. Although Denmark appears to have escaped, recent developments suggest a bubble is on the way.

Despite the figures and bubble narrative, the Nordic central banks appear to have little appetite, to raise rates, favoring growth and full employment. Nevertheless, they will have to rein inflation in at some point, raising rates. To mitigate a potential crash, we can expect to see the introduction and more widespread availability of longer-term mortgages: 40, 50 and even 100 years. Sweden and Japan already have 100-year intergenerational mortgages. By Nick Kamran, Letters from Norway.

And America has become “Landlord Land.” Read… So Who’s Pumping Up this “New Normal” Housing Market?